UNIQ Macro Summary – Q2 2023

UNIQ Macro Summary – Q2 2023

The stock rally coincides with investor sentiment hitting the highest levels since 2021.

Over the last quarter we have been working closely with a macro manager in an effort to integrate some of their AI models into our asset allocation thoughts. Deuterium Capital, based in the US with offices in Zurich have developed over time a quantitative model used by many institutional investors.

The synergy and key driver into utilising this research is that the quantitative models used are fundamentally driven by both inflationary and thereafter macro statistics. The models therefore offer us some insight into early detection of market directions and trends.

The modelling and interpretation detected early risk warnings for market corrections in 2022, thus models were underweight equities Q4 2021. Followed by trend and price signals in Q2 2023 indicating shift in monetary policy, strength of balance sheets and early entry valuation points.

Executive Summary

Equity markets are undoubtedly in a bullish mood, with positive market sentiment and a broadening out of the rally in stock prices in recent weeks.

What was a narrow rally in stocks during the first half of 2023, with a small number of large technology names dragging stock indexes up, has widened to include many other index constituents across different sectors of the economy.

Better than expected economic data releases and lower than expected inflation prints have supported this broadening out of the stock rally.

The stock rally coincides with investor sentiment hitting the highest levels since 2021. This is an increasingly popular rally with wider participation from retail and institutional investors alike.

Measures of positive / negative surprises on economic data are at their highest level in two years, indicating consistent beats on expectations. This has historically been a positive lead indicator for short-term stock returns.

This is an increasingly popular rally with wider participation from retail and institutional investors alike.

Higher asset prices have two important short-term effects on the economy that we should consider.

First, it makes those consumers who own stocks feel more confident. The asset side of their balance sheets is going up and so they feel more confident to spend a greater portion of their disposable income and save less. This extra spending hits the economy quickly. We are already seeing this effect in consumer sentiment data from the US, with some measures hitting two-year highs.

Second, it acts as an effective loosening of financial conditions. Much like a central bank cutting interest rates has a lagged effect on boosting the economy via a lower cost of debt, a rising equity market has a similar effect of acting to make equity financing easier and cheaper for companies. Easier access to capital, whether sourced via debt or equity issuance, is stimulative to the economy.

In both cases, the above factors are inflationary. This is something investors and market participants should be mindful of in the coming months.

In the meantime, however, disinflation and bullish market sentiment are clearly the order of the day, and investors should consider tactical participation in this rally while it lasts.

This tells us that the market rally may become more discriminatory as it goes on. Popular stocks trading on very high valuations (like Netflix and Tesla) may be prone to corrections in price on news-flow, even if that news is only slightly worse than expected.

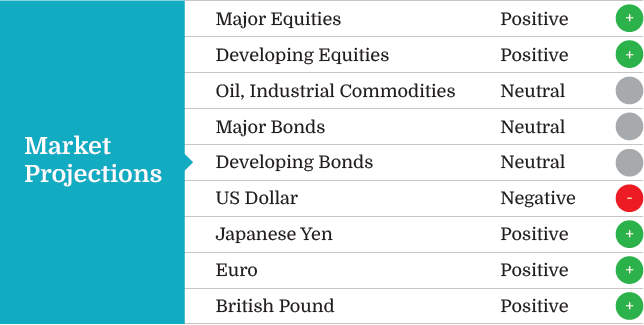

Risk asset valuations likely will continue higher in Q3 2023, finding support from lower worldwide inflation and the initial signs of an upturn in global output. Major bond markets will benefit from further falls in producer prices and subsiding headline inflation signalling that the pace of central banks tightening will slow significantly or stop.

Higher global aggregate demand and an unexpectedly strong expansion in world factory orders likely will lift risk asset performance during the quarter. Equity valuations will rise to reflect upside revisions to corporate earnings projections upon improving global financial conditions and higher global growth.

Investor anticipations of an eventual Federal Reserve shift away from monetary tightening likely will continue keep the US Dollar low against its principal counterparts, while a bottom in the global business cycle, along with improving financial conditions worldwide, will support risk asset valuations, in particular those of major non-US equity and developing market shares.

Economic outlook – Q3 2023

In Q3 2023 US fiscal, monetary and immigration policies probably will have the US Dollar exchange rate stabilizing at a lower rate. The increase in US government debt ceiling and subsequently debt/GDP from 82% to 137%, are indicative of structural currency weakness not fully reflected in present USD exchange rates. These structural factors likely probably will keep the US Dollar exchange rate lower than might be expected in the first stage of a worldwide economic recovery.

The high US headline inflation that brought real wages negative and lowered US disposable income growth is headed down quite rapidly. US producer prices and goods prices already have fallen below their levels of a year ago, and the rental inflation figures pushing up headline CPI now are negative as well. Lower inflation will boost US consumption and retail sales growth, even as lower commodity prices favour a move to expansions in global factory orders, durable goods, and exports.

As outlined in our macro review of early June, the indicators are becoming clearer hence the anticipation for optimism:

1. Higher than anticipated global demand with strong factory orders

World Inflation will continue subsiding sufficiently during the quarter to bring forward investors’ expectations of when global central banks will stop raising directed interest rates, even as global output will begin to expand. Lower major market bond yields in Q3 2023 will have begun to create much improved global liquidity conditions, in particular benefitting risk assets that are favoured in global cycle.

2. Core inflation cooling but set to gradually decline

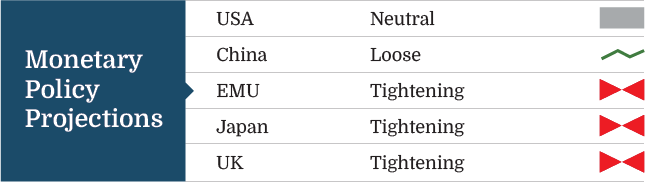

Central banks have continued to announce further expected monetary tightening and to implement significant rapid, rate hikes. Lower US price pressures, and subsiding headline CPI elsewhere, may have investors again anticipating a halt to directed rate rises. While the US central bank pauses to assess by how much domestic inflation will lag policy effects, the ECB and BoE may have to take into account the external dampening effects on their domestic price levels that come from their higher exchange rates versus the USD.

3. Labour market remains resilient against economic slowdown

Lower energy prices lift the growth outlook

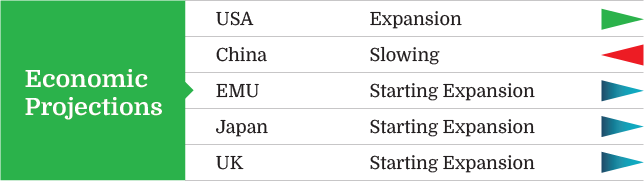

In Q3 2023 the US and European economies will shift to expansions in aggregate demand and production growth, while in the Far East industrial activity will begin to recover in line with higher worldwide exports. The Chinese economy nonetheless looks to grow at very low expansion rates for both production and consumption compared to previous cycles.

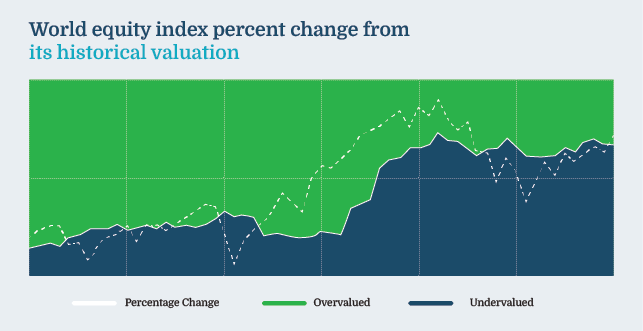

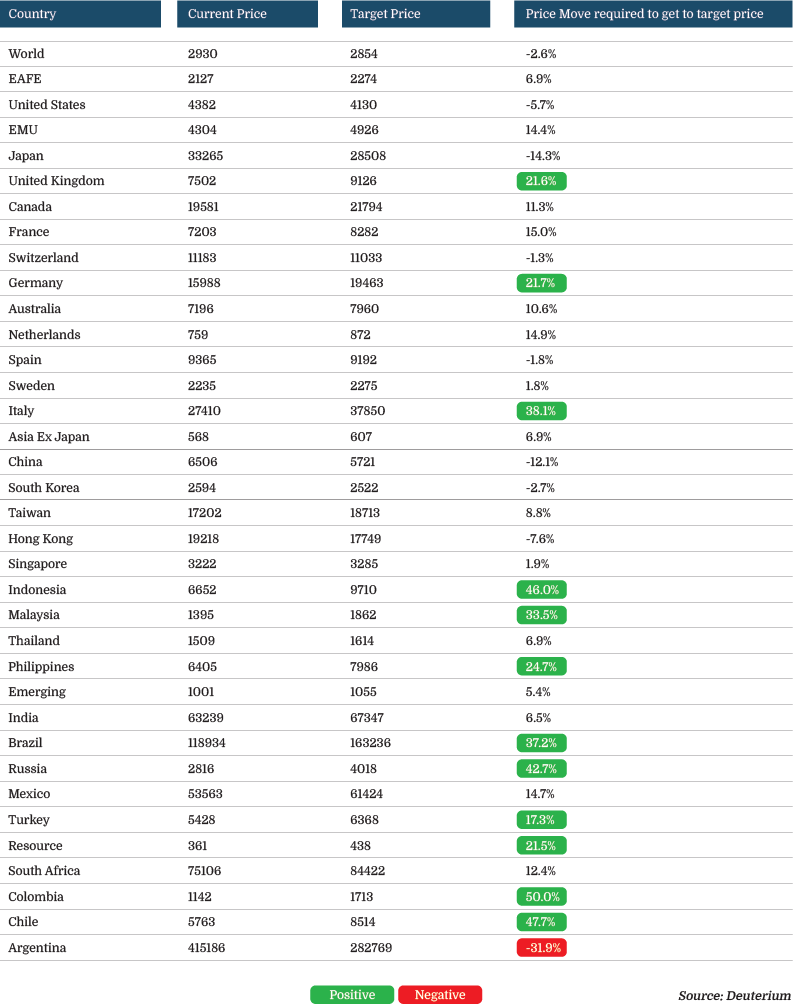

Valuation remains king, in our view, and should remain the focus of investors navigating this market.

Growth in corporate earnings, cash flows, and dividends has left most major markets below fair value compared to their historical averages.

US equities show as overvalued, with most other major markets except those of China and Japan well below fair value. UK, EMU, Far-East, and Emerging market equities show very attractive valuations.

While the inverted US yield and falling leading indicators are calling for an eventual US recession, on the contrary, projections across the consumption, investment, production, and price surfaces, country by country for all the regions, outline for Q3 2023 the start of at least a temporary recovery in global growth. They suggest that the sum of corporate balance sheet effects on investment, improved equity valuations, greater household liquidity, and higher household wealth effects on consumption will outweigh the negative effects from higher interest rates.

Corporate bonds now yield only 0.12% above the Fed Funds rate. The lowest level since 2007, preceding the Global Financial Crisis.

Every time credit spreads were at historically suppressed levels, a hard-landing scenario followed. Perhaps this time is indeed different.

Moreover, the Fed’s policy stance should also be taken into consideration. As we have learned repeatedly throughout history, tightening monetary policies work with a lag and we are yet to witness a significant credit contraction that could lead to further economic issues.

Even the apparent strength of the labor market should be taken with a grain of caution. Historically

low unemployment rates have served as one of the most reliable contrarian indicatorsinhistory.

Major non-US and Developing Markets are very undervalued

US equities are overvalued compared with historical averages for standard measures, with shares in most US sectors above their five-year averages for prices compared to earnings, sales, book value, cash flow, and dividends. In terms of their valuation metrics, shares in the materials and energy sectors remain substantially below their levels for fair value, while two large capitalization sectors, information technology and communication services, after rebounds this year are above their five-year averages.

While US equity overvaluation gives a slight negative to world shares, 13 of the 34 equity markets under review show very attractive valuations at present, while only those of China and Japan among the majors are very expensive.

Inflation subsiding

In Q3 2023, slowing inflation rates will again bring down expectations for further monetary tightening and likely will leave interest rates stable or at somewhat lower levels worldwide.

Those lesser headwinds and the start of a global recovery will lead investors to lift current poor projections for equity fundamentals and corporate profits, and to look to better fundamentals during the coming quarter’s upturn of the global economic cycle.

Inflation rates will continue to decline sufficiently to alleviate remaining pressure on interest rates during the quarter, while commodity and energy prices may find a floor at the start of a global cycle rebound, even if China shows much slower growth than expected. Producer prices, now negative, lead consumer prices, while broad money supply growth leads overall inflation by two years. Given those measures, headline inflation will be headed down.

The way forward is active management.

Over the past three years, we have seen recession and recovery and are now close to recession again. Normally, an economic cycle takes seven to ten years. This fast-paced cycle requires an active approach to investment.

The good news is that we now see far more opportunities in markets than at the start of 2022. Bond prices have fallen as yields have risen, leaving valuations at their most attractive level in over a decade. In 2022, bonds and equities fell in tandem. However, this year we expect to see more usual trading patterns re-emerge, with bonds rising as equities fall and vice versa. This means that in addition to offering higher yields, bonds should also do a better job of protecting portfolios in the event of equity market volatility.

We reduced exposure to equities throughout 2022 but are now looking to add back to the asset class. We remain on the sidelines for now, however. Our key concern is expectations for corporate earnings. Analysts continue to forecast a slight rise in earnings in 2023, which appears overly optimistic as we head toward a recession.

We expect volatility to continue inequities so we prefer to tactically allocate via Long Short macro strategies. We should be bias to short duration models to help navigate risk on /risk off shifts. Early allocation to these strategies are more welcomed as costs of hedging have reduced significantly.

(The author of this article is Marcus Queree, Partner & Director of FundStream. Any information herein is only expressions and opinions. This document does not constitute an offer, an invitation to offer, or a recommendation to enter into any transaction, nor does it constitute investment advice. The information contained herein is confidential and reproduction of any part of this material is prohibited. If you are in any doubt as to the suitability of an investment you should always consult your financial adviser. FundStream does not receive any form of compensation for circulation of such material.)

FundStream provides independent investment solutions to professional advisors to suit their clients portfolio preferences. Our investor network of professional investors include: pension funds, family offices, fund of funds and wealth managers in Europe, Asia and South Africa.

ADDRESS

Kemp House

160 City Road

London EC1V 2NX

United Kingdom

CONTACTS

+34 95 11 221 96

+34 95 11 221 97

![]()

INFO LEGAL